Although there have been multiple new models about profit and corporate responsibility that have been adopted in the last couple of decades, such as the triple bottom line framework, profit generation is still a company's main legal duty to its shareholders.

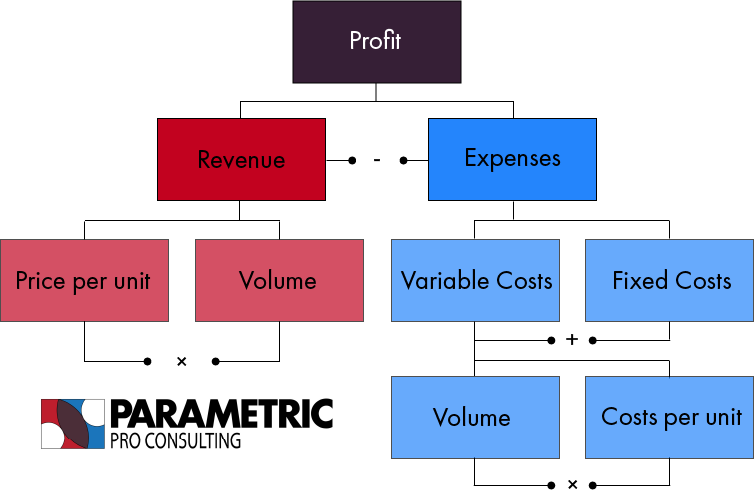

Maximizing profits depends on two main factors: maximizing revenues and minimizing expenses. The profit framework helps business decision makers organize their expense and revenue structures in order to maximize profitability. The framework is organized in a logic tree structure, which allows easier visualization of the granular details that make up revenues and expenses (see Figure 1).

On the revenue side, there are only two sub-components. The first element is the price that you are charging per unit for your product or service. If you are interested in how businesses often come up with their pricing models, you can read about that here. The other element in the revenue equation is volume. Volume is the number of units or services sold. To calculate revenue, you simply multiply the two elements. Every product or service line offered by your company will use this equation to calculate your gross revenue. From an organizational structure perspective, maximizing revenues is the responsibility of the sales and marketing teams.

Moving to the other side of the equation, expenses are broken down into two fundamental categories: variable costs and fixed costs. Variable costs are further broken down into two factors similarly to the revenue equation – volume and cost per unit. Fixed costs are expenses that do not change when the number of units sold changes. Examples of fixed costs include rent, advertising and promotion, insurance, and utilities. Oftentimes, when a company is experiencing shrinking profits, the first expenses that are cut are overhead (i.e. fixed costs). The other type of cost in the cost equation is variable costs. Variable costs are calculated by multiplying the number of units sold by the cost per unit. Once again, for every product or service line, this equation must be used to calculate gross variable costs. Gross variable costs plus gross fixed costs equates to your total costs. When looking at your organization's expense structure, the creation of expenses are usually generated by management and operations teams, where management creates the bulk of fixed costs and operations teams hemorrhage variable costs.

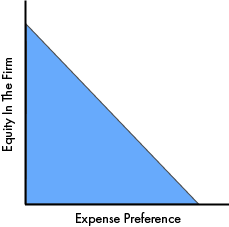

This phenomenon of management creating unnecessary expenses is a deeply studied field in economics. The most popular model that explains it is called “expense preference”. The expense preference model states that as managers earn more equity in a firm there tendency to indulge in their personal expense preference diminishes, since they begin to value the creation of profits for the firm more than their personal pleasure gained from expenses (see Figure 2). So, if you’re an owner or an executive of a company, offering options or RSUs (restricted stock units) to your managers may be worth investigating as a means to reduce expenditures.

Reducing variable costs is a little more nuanced matter. Oftentimes, it will involve doing process audits, where management will analyze the activities being performed for the production of goods or services. To learn more about how to analyze your company’s operations, you can read more here.

Profit generation is the goal of every business. It is what makes businesses sustainable and worth the risk associated with starting a venture.

If you liked this post, please consider sharing it with your network!

Check out our Business Strategy Frameworks guide for more useful tools.

Want to learn more and see how we can help your business? Book a free consultation call!

Are you interested in the consulting industry? Parametric Pro Consulting Foundations offers more in-depth knowledge on this article as well as several other topics to prepare you for a career in business and consulting. Check it out here!